October 18, 2025

by Laura Beltrán Figueroa

With the state’s official health insurance marketplace, Pennie, Pennsylvania cut the rate of those without medical insurance nearly in half over ten years, falling from 13.6% in 2013 to 7.1% in 2023.1 The new federal law reverses that progress. By 2034, between 645,000 and 846,000 Pennsylvanians are projected to lose coverage—the uninsured rate will double, premiums will rise sharply for nearly everyone in the marketplace, and safety-net providers will be pushed to the brink.

We recently released a long report covering these projected losses, the county- and district-level impacts, and the policy changes driving them. Here we summarize what we found.

Looking specifically at the sources of coverage loss, the new Medicaid work rules and frequent redeterminations account for between 375,000 and 576,000 people losing coverage, while Marketplace (Pennie) enrollment will drop by about 270,000 due to the rollback of subsidies and new enrollment barriers.

The Medicaid losses stem mostly from paperwork and reporting challenges. For example, a provision in the law requires enrollees to document 80 hours of work each month and complete renewal paperwork every six months. Even people who are working, caregiving, or have health conditions risk losing coverage if they miss a reporting deadline or paperwork notice. Another provision cuts the 90-day retroactive coverage period to just 30 days, leaving people with sudden medical needs uninsured for longer. And finally, the law requires some low-income enrollees to pay monthly premiums or higher copays, which creates new financial barriers, leading to both disenrollment and forgone care.

However, one of the most consequential provisions is the expiration of the enhanced federal health care subsidies. This issue is at the center of the current federal government shutdown with Democrats pushing to extend the subsidies to keep marketplace coverage affordable and Republicans refusing to authorize the funding, arguing instead for scaling back federal spending.

The enhanced premium tax credits were originally created under the Affordable Care Act in 2010. They were expanded temporarily in 2021 under the American Rescue Plan Act (ARPA) and then extended through 2025 under the Inflation Reduction Act (IRA). Before ARPA, subsidies were only available to those with income equaling up to 400% of the federal poverty line (about $120,000 for a family of four). ARPA removed that “subsidy cliff,” making middle-income families eligible, and capped premiums as a share of income: No one had to pay more than 8.5% of household income for a benchmark plan, with much lower caps for low- and moderate-income households. These changes meant millions of people either paid nothing (zero-dollar premiums) or much less out of pocket for coverage. In Pennsylvania, average marketplace premiums dropped by hundreds of dollars per month.

If Congress lets these subsidies expire, premiums will jump immediately for nearly everyone in the marketplace. Families above 400% of poverty will lose all assistance, while all families will see their share-of-income caps disappear. Unlike Medicaid enrollees, who face new copays and premiums, Pennie enrollees lose the cap that kept premiums tied to income—leaving them exposed to both higher premiums and the same out-of-pocket costs they struggled with before the benefit of the ACA. This means tens of thousands of households across Pennsylvania will once again face unaffordable premiums, leading to widespread coverage losses and higher uncompensated care costs for providers.

Pennsylvania expanded coverage through Pennie, which concluded its 2025 Open Enrollment Period with a record-breaking 496,661 enrollees.2 Pennie estimates that without the enhanced subsidies, monthly costs for enrollees will increase by an average of 82%.

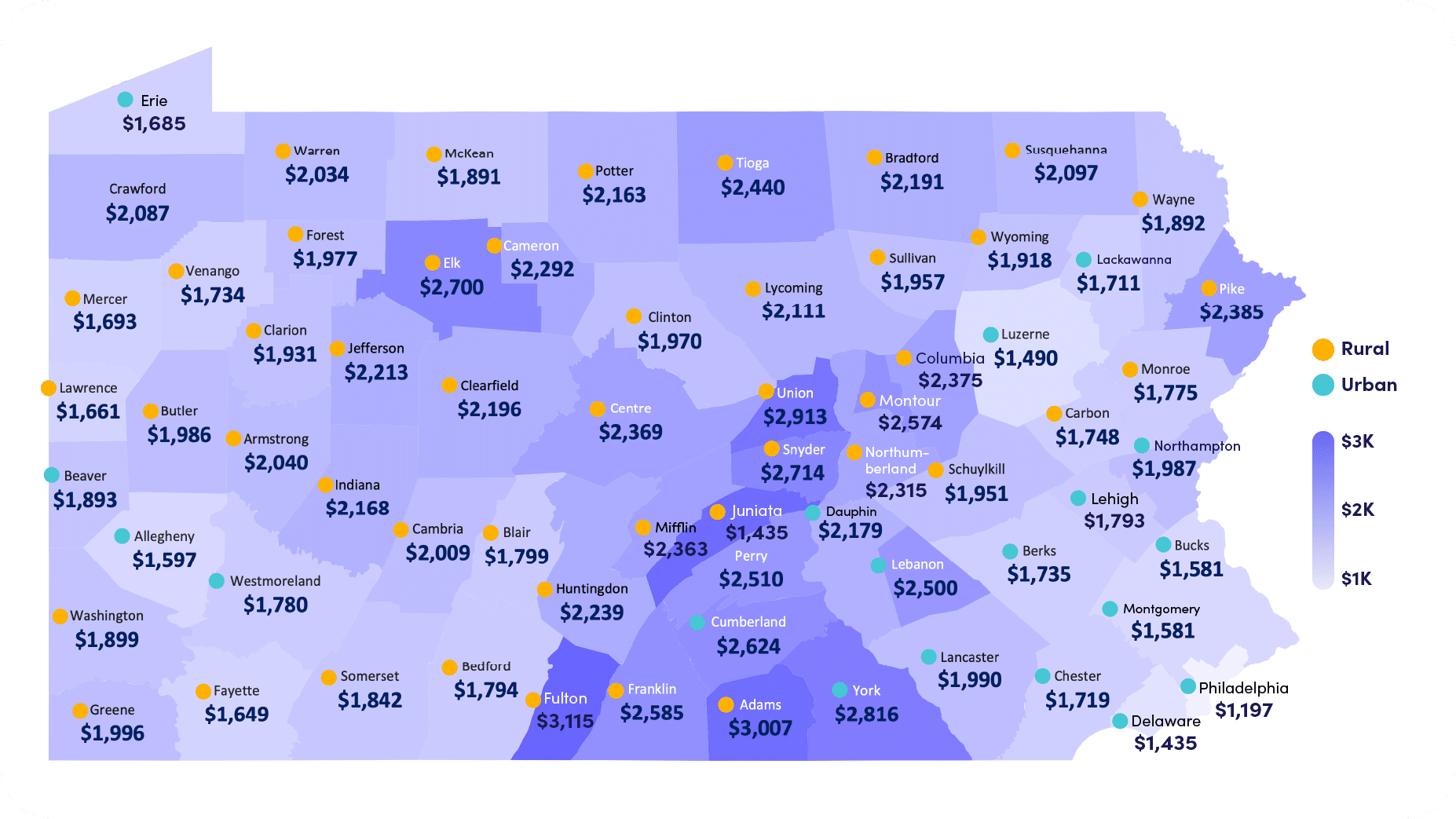

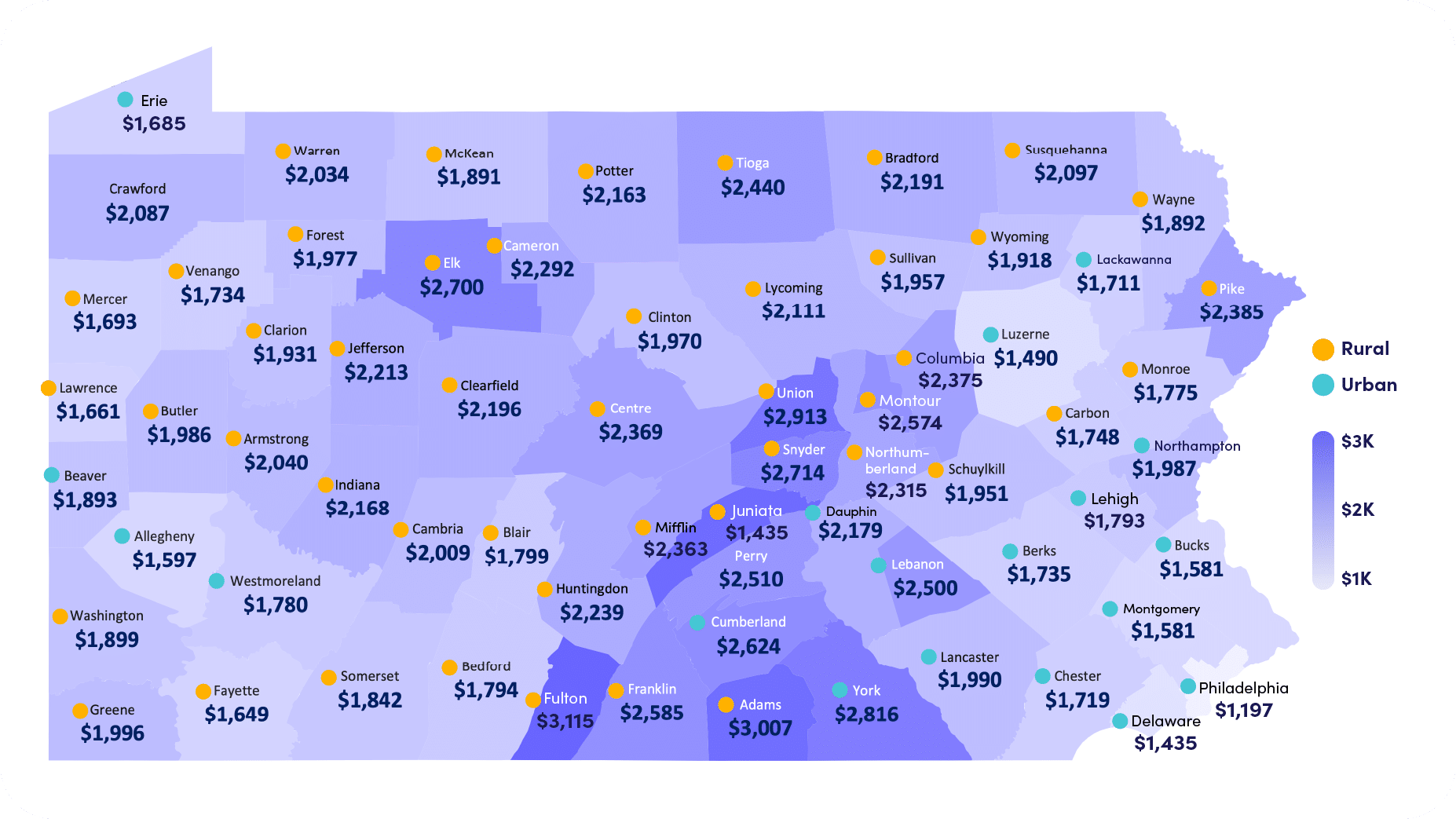

While a large portion of Pennsylvanians will technically remain eligible for coverage, county-level data show just how unaffordable it becomes. Average annual losses in federal premium tax credits range from $1,197 in Philadelphia County to more than $3,100 in Franklin and Adams Counties. In many rural counties—including Elk ($2,700), Snyder ($2,714), and York ($2,816)—families stand to lose between $2,500 and $3,000 a year in support. By contrast, urban counties such as Allegheny ($1,597), Montgomery ($1,581), and Delaware ($1,435) face smaller but still significant losses. If anything, the gap between rural and urban counties will widen since rural households already face higher premiums and have fewer employer-based coverage options.3

Source: Pennie, “Spotlight on Affordability,” accessed October 3, 2025, https://pennie.com/wp-content/uploads/2025/01/Average-annual-loss-of-advance-federal-premium-tax-credits-per-policy.png

{kind=link}